Type the phrase rebeca mingura credit one lawsuit into Google and the tone feels dramatic. Settlement numbers appear. Posts hint that thousands of Credit One customers may receive money. The story sounds settled.

The court file tells something different. The case exists. It sits in federal court. Yet the public record does not match many of the bold online claims.

That difference matters. Legal facts move through filings and orders, not social media captions.

The Case Lives in Federal Court

The lawsuit appears in the United States District Court for the Northern District of California. The official caption lists:

Rebeca Mingura

v.

Credit One Bank, N.A.

The Northern District of California handles federal civil disputes. That district covers major cities such as San Francisco, Oakland, and San Jose.

Federal courts deal with cases that involve federal statutes. This lawsuit centers on one specific federal law: the Telephone Consumer Protection Act, often called the TCPA.

The filing of a complaint starts the process. It does not prove wrongdoing. Courts require evidence. Judges review motions. Parties argue legal standards before anything close to damages enters the picture.

Many online summaries skip that part.

Why This Lawsuit Exists at All

The complaint alleges that Credit One Bank placed automated calls without proper consent. TCPA cases usually focus on robocalls, prerecorded messages, or use of automated dialing systems.

The Telephone Consumer Protection Act became law in 1991. Congress aimed to limit unwanted automated contact with consumers. The statute allows private lawsuits. It sets statutory damages at $500 per violation and up to $1,500 per violation if the conduct is willful.

Those numbers explain why settlement rumors spread so fast. People multiply the statutory amount across hundreds or thousands of calls. The math looks dramatic.

Courtrooms do not run on speculation. Judges require proof of consent issues, system design, and actual violations. Allegations alone do not produce payouts.

The Settlement Story That Circulates Online

One number keeps surfacing: $10.2 million. Some posts treat that figure as a confirmed outcome of the rebeca mingura credit one lawsuit.

Verified federal docket records do not show a final court order approving such a payout in this specific case.

Large TCPA settlements have happened in other matters. Capital One, Dish Network, and other companies have faced significant penalties or settlements in the past. Readers often merge those cases together. A prior settlement involving a different plaintiff does not automatically connect to this lawsuit.

Credit One has faced other lawsuits in the past, including cases that resulted in verified settlements, which are separate from the current federal dispute.

A true class action settlement leaves clear markers:

- A motion for preliminary approval

- A signed settlement agreement filed with the court

- A judge’s approval order

- Public notice procedures

- A claims administrator

Absent those documents, claims of confirmed multi-million dollar payouts remain unverified.

Individual Lawsuit or Class Action?

This question shapes everything.

An individual TCPA case involves one plaintiff. Any damages apply only to that person. No broad eligibility exists for other customers unless the court certifies a class.

A class action expands the case to represent a group of people who faced similar harm. Courts must formally approve that status. That process requires briefing, evidence, and judicial analysis.

Readers who want to know whether they qualify for compensation should check the docket for a class certification order. If the court has not certified a class, the lawsuit remains personal to the named plaintiff.

Search results rarely explain that difference. They imply wide eligibility even when no certification appears in the record.

How to Review Federal Court Records Without Guesswork

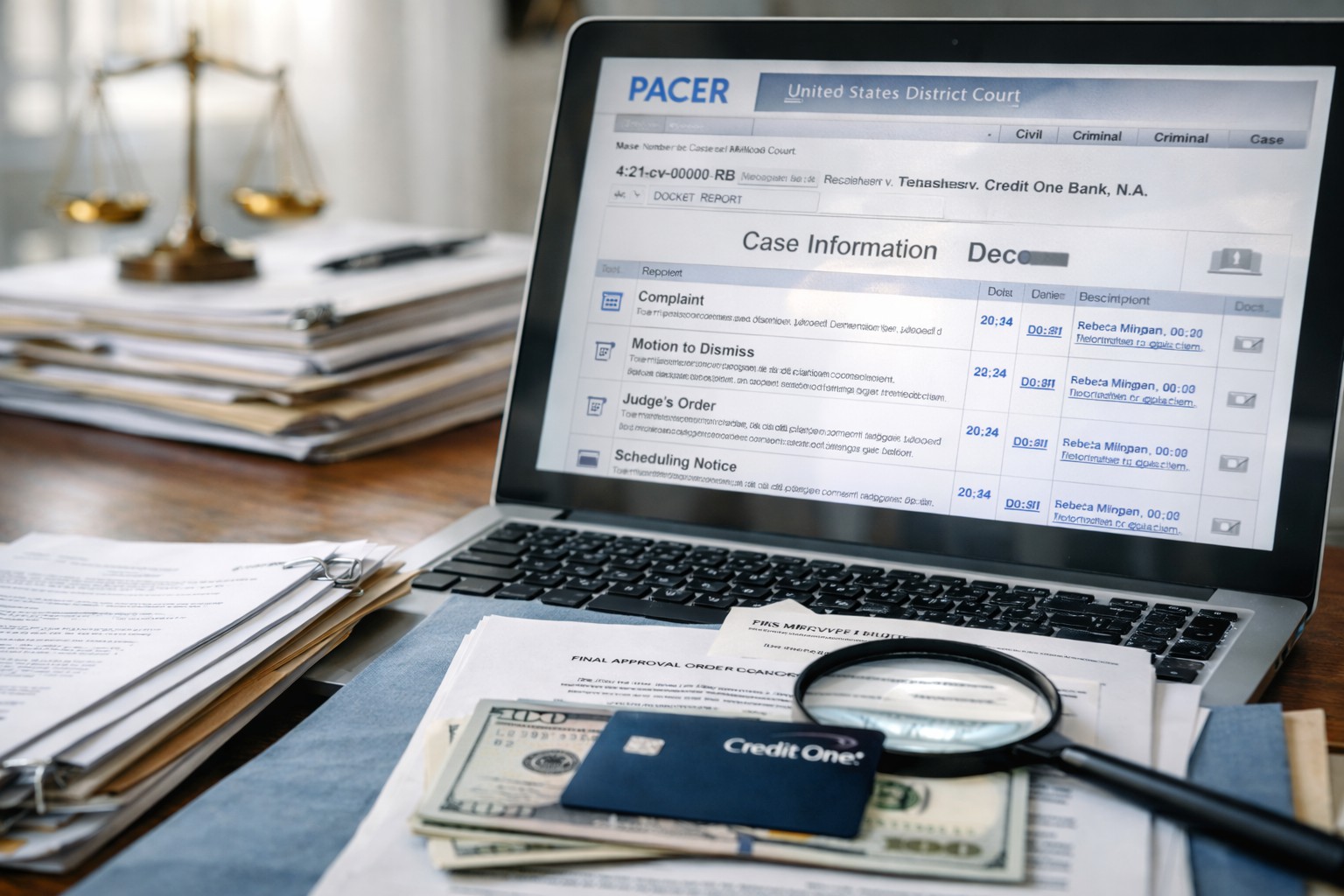

Online posts often make lawsuits sound dramatic. The truth sits in the court file. Federal civil cases appear on an official system known as PACER. This system keeps records from United States District Courts across the country. Anyone can search a case and see what the judge has received and approved.

Every federal case leaves a written trail. The first document is the complaint. That paper explains what the plaintiff claims happened. After that, the defendant may file a motion to dismiss. The judge then issues written orders that explain each decision. The court also posts scheduling notices that show deadlines and hearing dates. If the parties settle, the record reflects that step as well.

Large settlements do not happen quietly in federal court. A judge must review and approve class action deals. That approval appears as a formal order. The record will also describe who qualifies as part of the class and how claims must be filed. Clear deadlines and instructions appear in the docket.

When you see online talk about a payout, check the case file before you believe it. Look for a signed final approval order. Confirm that the court lists a settlement administrator. Review whether the order explains who can file a claim and when.

If those documents do not appear in the record, there is no confirmed settlement. Court files show facts in plain language. Headlines often leave out that detail.

Why Credit One Often Appears in Robocall Cases

Credit One Bank issues credit cards, often to consumers who build or repair credit. That business model leads to frequent account contact. Payment reminders, fraud alerts, and collection calls occur across the industry.

Automated systems sometimes manage those calls. Automated systems create legal exposure under the TCPA if consent rules fall short.

Credit One does not stand alone. Many financial institutions face similar claims. High call volume increases the chance of litigation.

Context helps. A lawsuit does not automatically signal systemic wrongdoing. It signals a legal dispute that a court must evaluate.

What the Supreme Court Changed in 2021

TCPA litigation shifted after the United States Supreme Court decided Facebook, Inc. v. Duguid in 2021. The Court narrowed the definition of what qualifies as an automatic telephone dialing system.

That decision raised the bar for plaintiffs. Companies can argue that their systems do not meet the statutory definition. Many post-2021 TCPA cases hinge on that issue.

The rebeca mingura credit one lawsuit operates within that modern legal framework. Older settlement examples may not reflect the current standard courts apply.

How These Cases Usually Move Forward

TCPA lawsuits often follow a predictable legal path, though outcomes vary.

First, the defendant may file a motion to dismiss. The court reviews whether the complaint states a valid legal claim.

Second, the parties exchange evidence through discovery. Call logs, consent forms, and dialing system details become central.

Third, settlement discussions may occur. Many cases resolve before trial.

Trial remains rare. Litigation costs push both sides toward negotiated outcomes.

The existence of a lawsuit does not guarantee trial, class certification, or public payout.

The Risk of Fake Claim Websites

High-profile lawsuit headlines attract scammers. Fraudsters create unofficial claim pages and collect personal information.

Consumers should never enter Social Security numbers or account data into a site unless:

- The court docket confirms a settlement

- A legitimate administrator appears in court filings

- Official notices reach consumers directly

No official notice means no verified claims process.

Caution protects personal data.

Why Viral Legal News Spreads Faster Than Court Orders

Legal disputes create clicks. Headlines travel faster than docket entries.

Writers sometimes repeat:

- Settlement figures from unrelated cases

- Incomplete summaries of complaints

- Assumptions about class action status

Court proceedings move slowly. Search trends move instantly. That gap creates misinformation.

Silence from major financial or legal news outlets often signals that no major ruling has occurred. Large federal settlements typically receive coverage from national media. Absence of coverage deserves attention.

Comparing Past Credit One Litigation to This Case

Credit One has faced other legal disputes. Some involved debt collection practices. Others addressed credit reporting or arbitration clauses.

Each case carries its own facts. Prior settlements do not determine future results.

Readers should avoid linking different lawsuits together unless court records show a direct connection.

The rebeca mingura credit one lawsuit stands on its own filings and judicial rulings.

If the Calls Keep Coming

Constant calls wear you down. You do not need to live with that. Take control early.

Write down every call. List the date, time, and phone number. Save voice messages. Keep text messages. Put everything in one folder or notebook. This record can help if you need proof later.

Send a clear message that tells the company to stop. Use email or certified mail. Keep a copy for yourself. A written request shows that you pulled back consent.

Look at your account terms. Some agreements allow certain contact. Make sure you understand what you accepted. If the calls do not stop after your notice, you can file a complaint with the Federal Communications Commission or contact your state attorney general. Good records can make a real difference if the issue grows.

What Actually Matters Right Now

The most reliable source remains the court docket. That record shows whether motions succeed, whether the case continues, or whether settlement discussions occur.

A filed complaint marks the beginning of litigation. It does not signal confirmed liability. It does not create automatic compensation for cardholders.

The rebeca mingura credit one lawsuit represents a live federal dispute governed by specific procedural rules. Real updates will appear through formal court orders, not viral reposts.

Readers who check the record gain clarity. Those who rely on rumor risk confusion.

Frequently Asked Questions

Is there a confirmed settlement in the Rebeca Mingura Credit One lawsuit?

Federal court records do not show a signed approval order for a settlement in this case. Without an official court order, payout claims remain unverified.

Can Credit One customers file a claim right now?

A claim process begins only after court approval and class certification. No official notice means there is no active claim program.

What law does this lawsuit involve?

The case involves the Telephone Consumer Protection Act. This federal law limits certain automated calls and texts without consent.

How can someone check real updates?

Updates appear in the federal court docket through PACER. Official filings provide accurate case status details.

What Readers Should Remember

Court files tell the real story. A lawsuit filing does not prove fault. Online posts often move faster than legal facts. Settlement claims require signed court orders and public approval. No official order means no confirmed payout. The rebeca mingura credit one lawsuit remains a federal case that follows standard legal steps. Readers who check verified records avoid confusion and false hope.