A lot of people do not search this phrase on a calm afternoon. They search it after a phone call, a new bill, or a contract reread that makes their stomach drop. Something feels off. The payment looks higher than expected. The deal terms do not match the talk in the showroom. The paperwork stack suddenly feels like a trap.

The phrase santander consumer western avenue nissan lawsuit connects two names that often sit on the same set of documents. One name is the dealership. One name is the lender on the account. That does not automatically mean both got sued for the same thing. People still search both because both appear on the deal.

A federal case tied to this search trend names Western Avenue Nissan and points to paperwork issues linked to financing submissions. A A public docket entry shows a case filed on May 8, 2025 in the U.S. District Court for the Northern District of Illinois as Burress v. Western Avenue Nissan, Inc., case 1:2025cv05106, with a claim type shown as RICO.

Industry summaries about the dispute also highlight something many readers miss. Coverage stated the suit described did not accuse Santander of misconduct. It described allegations focused on dealer conduct tied to loan submissions.

That distinction shapes how you should read the paperwork and how you should talk about it.

Do not get stuck on the lawsuit label

People see “RICO” or “lawsuit” and assume the story explains every bad car deal. It does not.

A lawsuit gives context. Your real leverage comes from your own documents. Your contract pages decide what you owe. Your credit file shows what got reported. Your copies show what you were told and what got signed.

So treat the lawsuit angle as a pointer, not a shortcut.

Start here if you think your loan file has wrong details

If you suspect someone changed your income, job, or housing numbers, you need control of the facts fast. No panic. No long arguments with staff. Keep it simple and direct.

Put your packet on a table and do three passes.

Pass one: identify the “money pages.”

Find the pages that show price, financed amount, APR, payment, add-ons, and totals.

Pass two: mark every signature and date.

Circle your signatures. Note which pages you did not sign.

Pass three: compare the numbers across pages.

Look for totals that do not match. Look for add-ons that appear in one place but not another.

A small mismatch can signal a bigger problem. A big mismatch usually means someone changed terms after you agreed to something else.

Quick Self-Check:

- Does your income match what appears on the credit application?

- Do the totals match between the buyers order and contract?

- Are there add-ons listed that you declined?

The dealer name detail that can confuse people later

Many people try to track records and hit a wall because the dealer name shifts across documents.

An Illinois appellate opinion dated May 13, 2020 notes that South Chicago Nissan was apparently doing business as Western Avenue Nissan. That matters when you pull older paperwork, ad screenshots, receipts, or court references.

Keep every version of the dealer name you see. Put it in your notes. Use the same name that appears on the page you reference. That avoids confusion if you request records later.

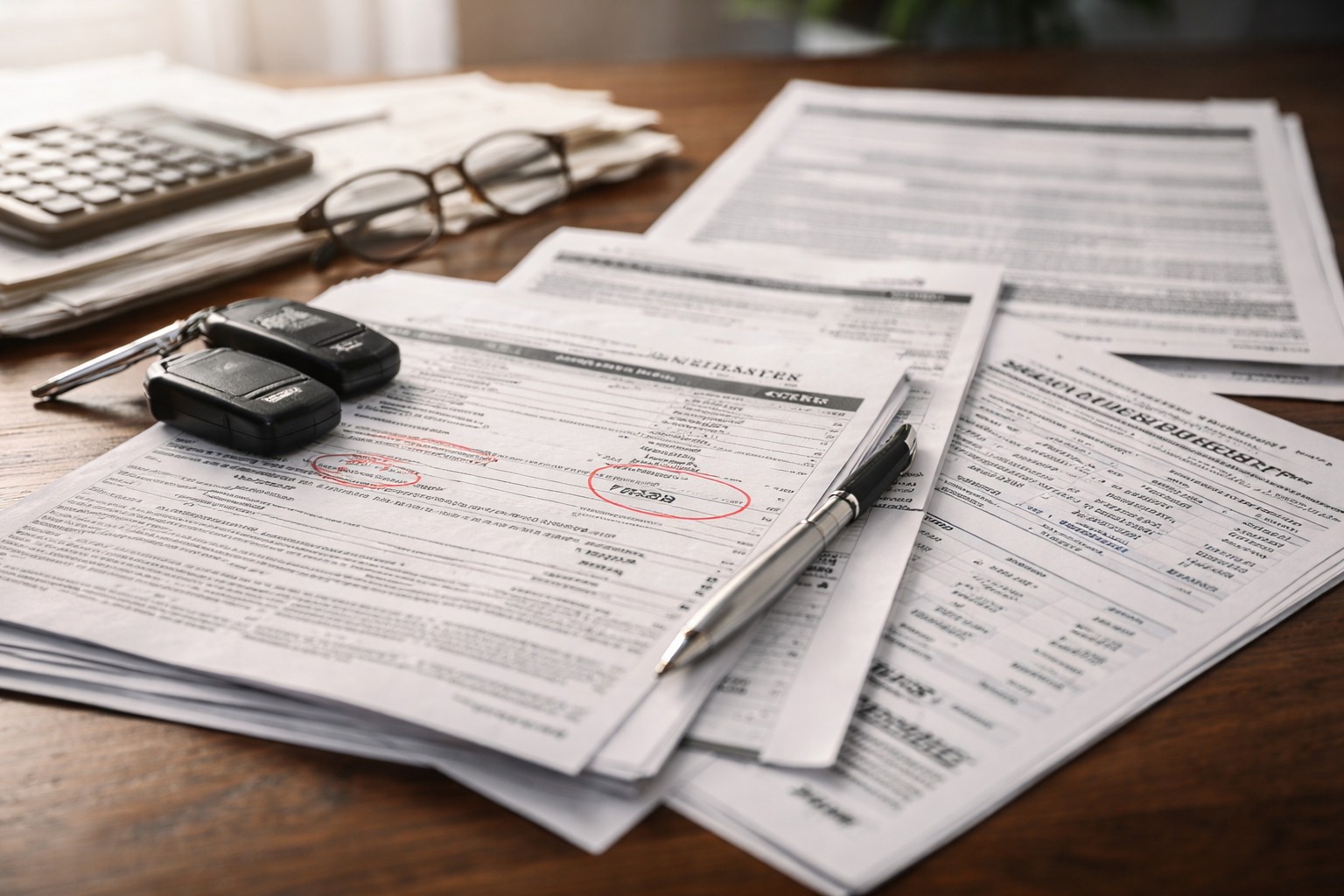

The pages that matter most when the deal “does not feel right”

Most buyers leave with a thick stack. Half of it has little value in a dispute. A few documents carry the weight.

The Retail Installment Sales Contract also called the RISC

This is the heart of most financed purchases. It usually shows:

- amount financed

- APR

- total of payments

- finance charge

- payment schedule

- late fee terms

- arbitration language

- assignment language to a lender

This is the page where a deal becomes real. Even a small change in totals or APR changes the entire cost.

The credit application copy

Buyers often never see the exact submitted credit application. That creates problems later. This page is where income and employment details appear. This is also where a buyer sometimes finds a job title, employer, or income number they never gave.

A practical tip that consumer lawyers repeat: ask for the exact credit application transmitted. Ask for the version sent to the lender, not a blank form and not a “summary.”

The buyers order and itemized price sheet

This page tells you what you paid for the car and what got added.

Look closely at add-ons such as service contracts, warranties, GAP, theft products, paint protection, and similar items. Check dealer fees too. If a fee did not appear in the first offer, ask why it appears now. “Market adjustment” lines also appear in some deals and can raise the price fast.

Truth in Lending disclosures

Many RISCs include these disclosures inside the contract. Some deals also add a separate disclosure page. Either way, TILA numbers should match the payment reality. If the math does not line up, treat that as a serious issue.

Conditional delivery or spot delivery paperwork

Some buyers drive off before final approval. Dealers sometimes call this “conditional delivery,” “spot delivery,” or similar wording. If approval changes later, the dealer may push a new contract with different terms.

This issue causes many “come back and re-sign” calls. Those calls often feel urgent on purpose.

Ad copy and screenshots

People ignore this evidence until it is gone. Ads change. Listings disappear. Screenshots help show what you saw at the start, especially if the dispute involves bait tactics or price shifts.

A consumer story tied to the same lawsuit narrative describes bait-and-switch pressure in a Nissan dealership context. That type of detail often becomes clearer when a buyer can show the original listing.

The problem buyers fear more than a high rate

Most buyers can accept a rate that feels higher than expected. What they cannot accept is a loan file that does not match what they said.

A typical auto finance process looks simple on the surface. A buyer gives income, job details, housing cost, and basic identity details. A finance office enters that into a credit application and sends it to a lender.

If someone changes those inputs, the buyer can end up with:

A loan they never would have accepted, if the real terms were clear.

A payment they cannot carry, month after month.

Credit damage if the deal collapses or turns into default.

Repossession risk if the payment fails.

Coverage tied to the Western Avenue Nissan dispute described allegations that employment and financial details on credit applications got misrepresented in submissions tied to Santander Consumer USA.

Allegations are not verdicts. The fear behind them still matches what many buyers experience in everyday disputes.

Red flags that show up inside “bad deal” paperwork

You do not need legal training to spot certain patterns.

Income numbers that look inflated compared to what you told the dealer.

A job title or employer name you never gave.

A housing payment listed much lower than your real amount.

“Self-employed” checked when you never said that.

A co-buyer added with no clear consent.

Add-ons that show up after you declined them.

Two contract versions with different totals.

A rushed re-sign request after you already took the car.

Compare totals line by line. Compare the buyers order to the contract. Compare the contract to any later contract you signed. If the numbers move, ask why.

Real-World Scenario

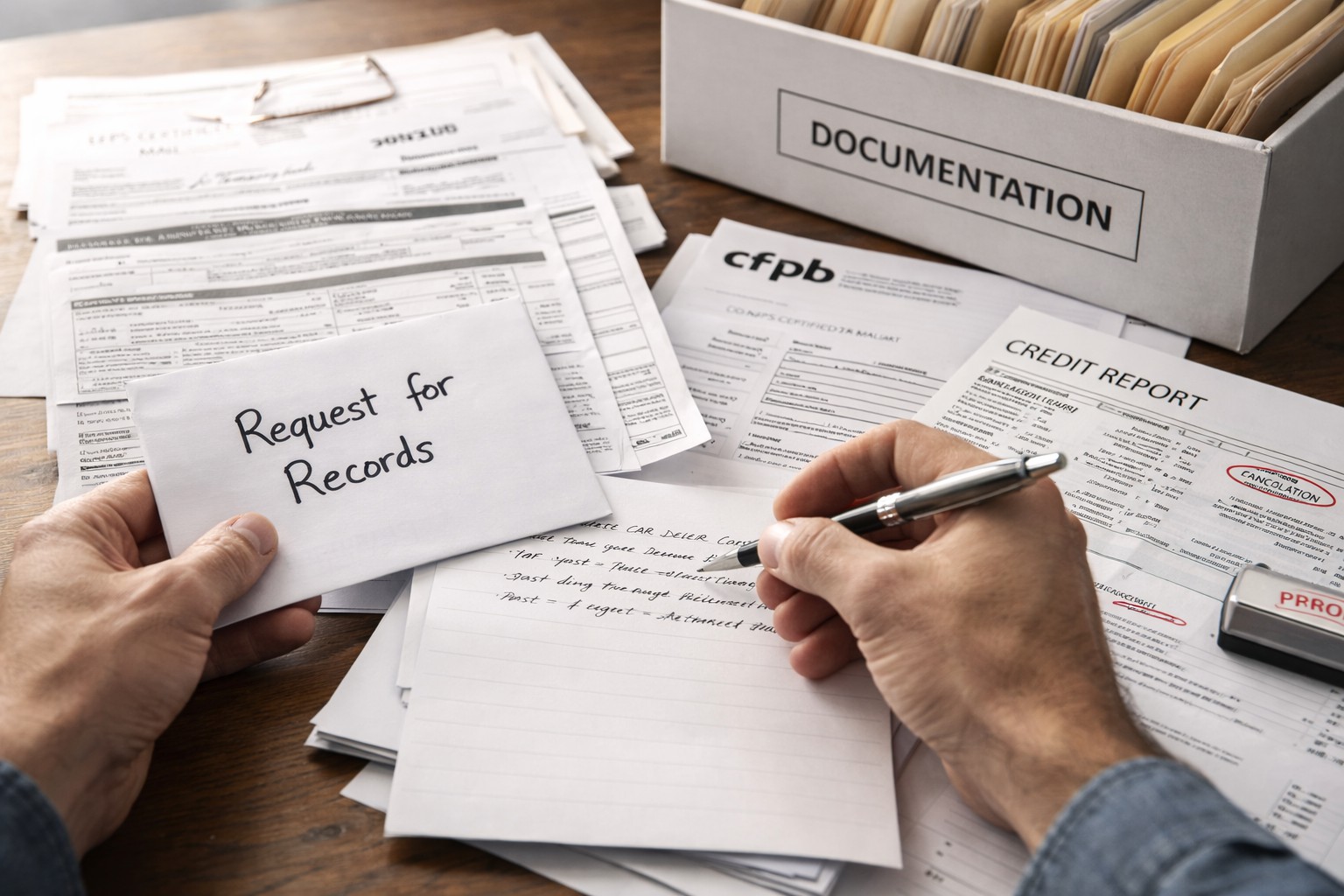

A buyer in Illinois reviewed his loan papers three months after purchase. He noticed the income listed on the credit application was higher than what he actually reported. The payment seemed manageable at first, but the inflated income helped approve a loan he would not have qualified for under his true numbers.

He requested a full copy of the submitted credit application from the dealer and compared it to his original documents. The differences became clear. That written request created a record and helped him organize next steps.

The key lesson: small numbers on paper can change the entire cost of a deal.

Why Santander appears in the search phrase even when the dealer sits in the lawsuit

Many readers assume the keyword means “Santander got sued.” That is not always what the search phrase reflects.

The docket summary people cite centers on Western Avenue Nissan as a defendant in the 2025 federal case. Industry-post summaries about the same dispute stated the suit described did not accuse Santander of misconduct.

So why do people type Santander in the same search?

Because Santander is often the lender name on the buyer’s paperwork and account. Buyers search the lender and the dealer together since both names sit in the same packet and both show up in calls, letters, and credit reporting.

Your article should make that clear. A lender can appear in a story even if the claim focuses on dealer conduct.

Rights buyers usually have when paperwork looks wrong

People want actions they can take. They do not want theory.

Ask for your records and do it in writing

You can request copies of your signed contracts and related documents from the dealer. You can also request account and payment records from the lender.

A clean approach works best:

- Ask the dealer for the full deal jacket copy.

- Ask the lender for the full account history and file notes tied to the account.

- Keep proof of your requests.

Dispute credit reporting with organized facts

If a deal breaks down, buyers may see late marks, charge-offs, or repossession notes. Federal credit reporting rules allow disputes. An organized dispute works better than an emotional one. Attach clear proof. Keep your language tight.

Challenge deceptive sales practices under state laws

Most states have consumer protection laws that cover deceptive practices. Illinois has its own consumer fraud framework. Your post can keep it general and note that state law controls many dealer conduct claims.

Cancel some add-ons in many situations

GAP, service contracts, and similar add-ons may have cancellation terms. Many buyers never use them and never cancel them. In some cases, a cancellation reduces the balance or triggers a refund path.

Know the repossession rules before you react

Repossession has rules even when a buyer falls behind. Notice requirements and sale requirements often apply. “Breach of the peace” disputes show up across repossession cases. Your readers should understand the risk before they decide to stop paying.

One habit that prevents a lot of damage

Here is the mismatch that hurts buyers most.

The buyer focuses on the monthly payment. The finance office focuses on the backend. That gap lets add-ons and term changes slip in when the buyer feels rushed.

A better habit is simple.

Ask to see the amount financed, the total of payments, and the itemized add-ons before you sign. Ask again before you re-sign anything.

A refusal is a warning sign. A rush is another warning sign.

Complaints can help but only after you lock down your proof

A lot of people file a complaint too early. They do it before they can show what went wrong. That weakens the complaint and wastes time.

Get your facts in order first. Save:

- Ad screenshots.

- Texts with the salesperson or finance office.

- Emails and lender notices.

- Bank statements that show income reality.

- Pay stubs or tax documents that show what you actually earn.

Then watch your credit report. Track how the account reports. Note any change in status.

After that, a complaint often becomes easier to understand and support with documents. People often use:

- State attorney general consumer divisions.

- State motor vehicle dealer licensing authorities or boards.

- The Consumer Financial Protection Bureau for lender-side product issues and complaint routing.

A CFPB enforcement action page describes a settlement tied to Santander’s GAP add-on product disclosures, with a page last modified January 2, 2024. That does not prove anything about a reader’s situation. It does show regulators pay attention to add-on disclosures in auto finance.

Older Santander settlement details people often mix into this topic

Readers sometimes bring up older Santander settlements when they search this keyword. Two items show up often:

A multi-state settlement announced in May 2020 tied to allegations about underwriting issues dating back to 2010, with a public statement posted by Santander on its investor relations site.

A public settlement site tied to that multi-state attorney general settlement and related press materials.

These items can add context. They are not the same thing as the Western Avenue Nissan dispute. Your guide should keep them separate so readers do not mix different matters into one story.

The same problem shows up in different clothes at different dealers

A paperwork dispute can look like several patterns:

Price changes after arrival that feel like bait-and-switch.

Conditional delivery that turns into a second contract with worse terms.

A yo-yo pattern where the buyer returns under pressure to re-sign.

Add-on packing that inflates the financed amount.

Credit application inflation that makes approval possible.

These patterns show up across brands and cities. The dealership name may change. The tactics often stay the same.

Questions people ask when they stop trusting the deal

Most readers do not ask “What is RICO.” They ask practical questions.

Can I unwind the deal

Sometimes yes, sometimes no. State law and contract terms control it. Spot delivery paperwork can matter.

Can I return the car and walk away

Some deals allow it. Some deals do not. A return without written terms can still leave a balance.

Can I sue

Possibly. Many contracts include arbitration clauses. Deadlines can apply. A local consumer lawyer can tell a buyer what fits their facts.

Should I stop paying

Stopping payments can trigger repossession and credit harm. Buyers should understand that risk before they act.

Similar allegations appear in the Lola tampons lawsuit details, where ingredient transparency and safety claims became central issues.